Four Corners of the Room

The space was divided into four distinct sections. One represented Basic Need, while another was designated for Want. A third area stood for items considered Sometimes Necessary, and the final corner was for those deemed Not Required At All.

The group congregated in the middle, waiting for the exercise to begin.

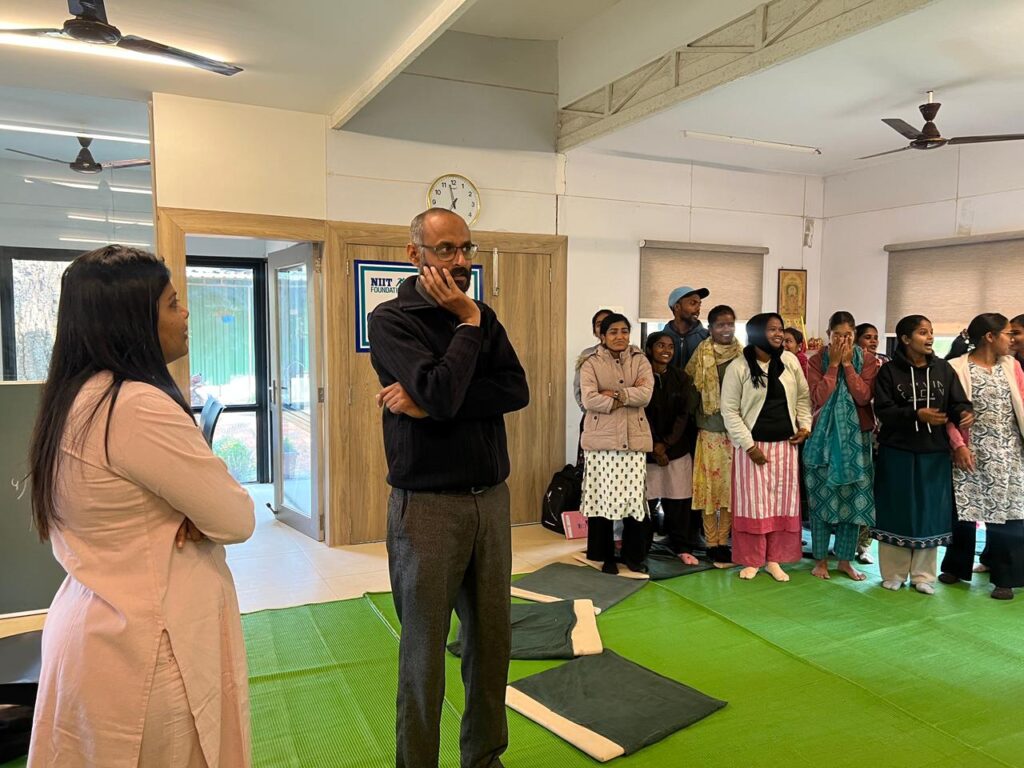

Most of those present were Earth Focus Foundation’s Shiksha Preraks and Samuday Preraks—individuals whose work spans supporting children’s education in Anand Ghars to engaging villages in restoration and livelihood initiatives. For a significant number of these young professionals, this role represented their first encounter with a steady monthly income and the new financial choices that follow.

Leading the sessions was Vrushti Sheth, a renowned Mumbai-based financial planner who established Vrushti Sheth Capital Services. She had been invited by the Foundation to lead a financial literacy workshop designed for the ground staff, bringing a structured curriculum that touched upon the mechanics of budgeting, banking, and insurance, alongside the complexities of investments and long-term planning.

Sheth called out the first item.

“Milk.”

Most moved towards Basic Need, though a few walked towards Sometimes.

Next came an Android phone.

This time the group split.

Then came an iPhone.

Laughter broke out as people scattered across the room. Some immediately walked towards Want. Others shook their heads and crossed to Not Required At All. A few stood hesitating in the middle before choosing a side. As participants began defending their choices, the conversation quickly moved beyond the phone itself. For some, it represented an unnecessary expense. For others, it raised a different question: at what point does a useful tool become a luxury?

The exercise looked simple. Yet people were making very different choices. What one person considered essential, another viewed as unnecessary. What seemed obvious to some depended entirely on circumstances for others.

For Sheth, that was precisely the point.

“No finance rules are the same for everyone. Before taking any financial decision, you have to understand your own situation.”

As participants debated their choices, the conversation began raising a different question: how do people learn about money in the first place?

Starting With What One Already Knows

Long before anyone teaches budgeting or financial planning, individuals are already learning about money through everyday life. They watch adults negotiate purchases in markets. They hear conversations about loans, school fees, harvests, household expenses, and other major family decisions.

For a significant number of the Shiksha Preraks and Samuday Preraks, a steady monthly salary itself was novel. This shift brought with it a fresh set of obligations—balancing household needs, investing in the education of younger siblings or their children, and navigating the practicalities of saving while assisting parents with the sudden, often unforeseen, expenses of life.

Rather than beginning with financial terminology, Sheth asked participants to think about expenses they were already managing.

“A few said that after we started earning this salary from Earth Focus, we now have our own scooter and are paying the EMI,” she recalled.

The scooter quickly became more than a vehicle. Participants began discussing fuel costs, maintenance, loan repayments, and the practical realities of travelling across villages spread over large distances. Some described the freedom that came with owning a vehicle for the first time. Others spoke about the pressure of monthly repayments.

Similar conversations followed about mobile phone recharges, new clothes purchased during Diwali, travel expenses, a birthday celebration, and the cost of replacing a damaged phone screen.

These were not hypothetical exercises. They were decisions participants were already making.

What began with familiar purchases gradually opened up larger questions about how families plan, prioritise, borrow, save, and respond when circumstances change. The exercises also revealed that not everyone had been invited into these conversations in the same way.

Learning Money Unequally

The differences became especially visible during one exercise on household budgeting. Participants were asked to prepare a rough account of monthly household expenses and think through how money entered and left a family over the course of a month.

Some completed the exercise comfortably. Others struggled.

Several women participants explained that conversations around household income, savings, expenditure, or debt rarely involved them. Fathers managed finances. Brothers or husbands accompanied family members to banks or markets. Major financial decisions were often discussed elsewhere.

Many of the women were already managing significant responsibilities within their households. They supported family members and contributed to decisions affecting education, healthcare, and household wellbeing. They knew the details of household spending intimately — groceries, school supplies, medicines, festival preparations — yet were often excluded from discussions about income, savings, debt, or long-term planning.

The exercise brought into view a gap that had existed for years. For some, this was the first time they had been asked to map a household budget from beginning to end.

Yet these same women were often among the most engaged participants in the room.

“The women often displayed the greatest curiosity,” Sheth observed. “They possess a genuine desire to engage and understand. Yet, despite this eagerness, they found themselves unable to finish the exercise because they had been traditionally sidelined from such financial matters within their own homes.”

The workshop also offered another kind of exposure. Many participants were interacting for the first time with a woman whose profession centred on financial planning, taxation, investments, and wealth management. For young women in the room, particularly those at the beginning of their careers, the encounter expanded the range of possibilities visible before them.

More Conversations Beyond the Curriculum

The sessions covered budgeting, savings, borrowing, insurance, banking, and financial planning. Yet the most animated discussions often emerged when participants began connecting these ideas to their own lives.

An Android phone could be essential for one participant and unnecessary for another. A loan that helped one household manage a difficult period could create problems for another.

As the sessions progressed, people increasingly brought their own questions into the room. Some wanted to discuss loans. Others asked about insurance, savings schemes, or future plans.

The conversations continued long after particular exercises ended. Money remained the subject but people compared experiences, debated choices, and returned repeatedly to questions that had no single correct answer.

“What is truly necessary and what can wait?”

“How do families decide?”

“Which traditions continue to shape financial decisions?”

“What responsibilities arrive with a first salary?”

“Which expenses seem unnecessary to one generation but indispensable to the next?”

“Who gets invited into conversations about money, and who remains outside the room?”

These questions do not disappear when a workshop ends. They continue inside households, among friends, in workplaces, and across communities.

Perhaps that is why the most memorable parts of the training were not always the exercises themselves. They were the conversations that followed.